The future is online. Actually, the present is online, and the future more so. The COVID-19 pandemic, and the constant refrain about the “new normal” prove that not only is internet access vital to 21st century life; high-speed access is a necessity. It is no longer enough to just have internet access; one must have quality access. And that is going to depend on open access fiber.

Being a full participant in the world will eventually depend on access to gigabits of broadband capacity. That capacity will depend on fiber optics. Over the years, EFF has researched and advocated for policy changes at the local, state, and federal levels—all towards the goal of delivering universal fiber to everyone in the country. Part of that work has required us to look back at the mistakes made in the past, how they’ve led to the problems of today, and how to avoid making the same mistakes in the future.

One of the biggest mistakes has been overly relying on large, publicly-traded, for-profit companies to deliver universal access. For decades, policymakers have given billions in subsidies to the likes of AT&T, Comcast, and Verizon to build out their networks, with the goal that the existing companies serve everyone. These companies were gifted with countless regulatory favors designed for and often by the largest corporations. Their lobbyists were given front-row status in guiding policy decisions in Congress, state legislatures, and the Federal Communications Commission. In return for nearly two decades of favoritism, still more than half of the country lacks 21st century-ready broadband. Millions in the United States remain unserved.

A new study, funded by EFF, explains why that is and how we can reorient our public investments into broadband infrastructure able to connect all people to the gigabit future. Put simply, the biggest mistake in broadband policy has been in subsidizing broadband carriers, hoping they would build infrastructure, as opposed to focusing directly on future-proof infrastructure development. As a result, when we spend $45 billion—and counting—on supporting any service reaching a bare minimum metric of 25/3 Mbps (the federal definition of broadband), we fail to build long-term infrastructure, while squandering resources on dated copper, cable, and long-range wireless solutions. With another $45 billion potentially getting queued up by Congress, now is the time to rethink how we spend those new funds, and focus not on getting just any service to people, but on getting infrastructure to them that will sustain us for decades.

What is an open access network and why must it be fiber?

A true open access network (also known as a wholesale network) is an entity that does not sell broadband services, but rather offers the wires that enable anyone else to sell broadband services, along with other data applications. In other words, a truly open access network is one of infrastructure. And then, anyone else can build on that existing infrastructure to become a broadband service provider.

These types of entities have existed for years in the EU, thanks to a regulatory scheme that incentivizes them. They have been deploying fiber optic infrastructure to the EU member nation-states. Fiber is their choice because it is a future-proof transmission medium that will handle internet growth for decades, without new investments. So, while fiber costs a lot at the outset, it will only become more valuable over time. As our study found, this results in what are known as patient capital investors—investors willing to wait the requisite number of years before an investment starts to pay back.

No one doubts that everyone will need greater amounts of data capacity as the internet continues to evolve and grow. A pure infrastructure provider, like an open access network, will not be looking to reap its rewards from broadband customers, but from selling access to a multiplicity of providers, giving it an incentive to build the fastest, most future-proof infrastructure possible. Furthermore, it has an incentive to lease space on its network to many different broadband providers, in order to recoup its costs. That will create competition in an area where it is sorely lacking. Many ISPs will now have the ability to offer plans in new markets, and consumers will be able to pick the one that they like best.

The future will create more services that require high-speed broadband. To build a network that can provide for those needs and make money, an infrastructure provider will need to be able to offer more and more without having to constantly upgrade what its built. Right now, only fiber optic wires can do that. It cannot be replicated or replaced with other data transmission mediums, such as cable, wireless, and satellite. Fiber optic wires hold terabits of spectrum capacity, and we haven’t even invented the hardware that can make full use of that capacity yet.

In the long term, open access fiber networks are more efficient and able to reach more people than government subsidies.

The United States has ended up with slow, expensive, and non-universal internet access by relying on the wrong entities to build the country’s communications infrastructure. Large, private, vertically integrated (owning content production, telephone services, alarm systems, wireless services, and streaming) ISPs are burdened with attempting to achieve multiple goals in the chase for profits. Their mergers and acquisitions strategy has resulted in big telecoms accruing the most debt in the world, forcing them to seek ways to minimize investments. Every minute and dollar spent on the non-broadband services is a dollar and a minute not spent on upgrading and building infrastructure. In fact, it’s even worse: where a broadband provider is a monopoly, they have a guaranteed income to spend on the non-broadband services and no incentive to improve the broadband side. This multi-headed hydra approach negatively impacts their ability to focus on the core element of broadband access: rolling out next-generation fiber optics.

These giant legacy companies often tell policymakers and the media that financing fiber infrastructure is “too expensive” in order to avoid the actual truth, which is that it’s only too expensive for them. Once an entity’s only concern is to lay data transmission lines, the equation changes dramatically, according to our cost model analysis.

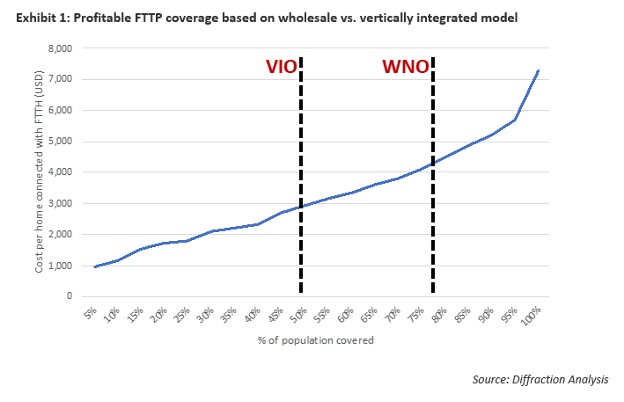

The truth is, with the appropriate amount of patience and a long-term investment strategy, universal fiber access is feasible. Provisioning fiber infrastructure on a wholesale model, which means selling capacity to all comers but not selling broadband service, makes it feasible to build out to large swaths of the United States where symmetrical gigabit and beyond demand exists or will exist in the future. When factoring in all the burdens (and risks) a vertically integrated ISP carries with it today compared to the simplified approach of an infrastructure-only deployment, our cost model shows that an infrastructure-only entity can deliver fiber optic wires to nearly 80% of the population for a profit while vertically integrated ISPs can reach at best only half.

In other words, if our broadband policy and subsidy dollars revolve around the premise that the AT&Ts and Comcast's of the world are the best or only solution to the problem of broadband, we’re doing it wrong. And it’s costing taxpayers a fortune. If our goal is to get fiber-optic connectivity to everyone, we need to change course and focus solely on entities delivering infrastructure. This will require a change in regulatory and public investment goals.

The Federal Communications Commission has to establish infrastructure policy, and states should prioritize building open access fiber networks.

Our model shows that an emphasis on open access infrastructure will yield tremendous savings to taxpayers by reducing subsidies, and expanding fiber access to tens of millions of more Americans stuck in cable monopoly markets. But our study shows that this will not happen on its own.

The Federal Communications Commission (FCC) needs to proactively adopt competition regulations that reduce risk to infrastructure providers in order to take full advantage of their efficiencies. Some examples of what the FCC could do include: identifying where accessible fiber is present through broadband mapping, ensuring that open access providers are given the same rights as AT&T and Comcast, and adopting rules that prevent predatory pricing by cable companies, who will want to prevent fiber deployment to preserve their monopolies.

Much of the focus of broadband mapping has been on identifying speed metrics, but not on the long-term viability of existing infrastructure. As a result, a speed-capped satellite connection is treated the same as a fiber wire with multi-gigabit potential. The FCC, particularly if Congress invests billions in broadband access, needs to help identify where future-proof capacity is lacking in order to better inform would-be investors of fiber opportunities.

However, given that open access providers are not traditional telecoms, they need to be given the rights of way and pole attachment, rights provided to Title II common carriers. Otherwise, they will run into the same problems Google Fiber did when AT&T withheld access to its poles in Texas. Lastly, many of the attractive long-term investment markets are going to be cable monopoly markets. However, if cable companies are allowed to engage in predatory pricing of broadband access to head off future competition, it will effectively undermine long-term fiber investment models. In other words, the FCC must adopt rules that prohibit cable companies from cross-subsidizing their monopoly markets with future competitive markets and require equivalency in pricing. If they are offering one market lower-cost high-speed broadband, they must offer that to all markets across their territory. But all of these suggested policies are contingent on the FCC restoring its authority over broadband carriers and reversing the deregulation that occurred with the Restoring Internet Freedom Order.